After three years of turbulence, can Bangladesh’s steel industry find its footing again?

The Great Slowdown: Three Years of Struggle

Bangladesh’s steel industry, once the pride of South Asia’s infrastructure boom, is now weathering one of the worst crises in its history.

According to India-based market intelligence firm BigMint, steel demand—a key indicator of economic health—has remained weak for three consecutive years. The firm projects that demand may take until FY2027 to normalize.

What began as a temporary downturn has evolved into a prolonged stagnation. From the aftermath of Covid-19 to the Russia–Ukraine war, global shocks have rippled through the domestic market.

Internally, the sector has been hit hard by political instability, currency depreciation, and banking dysfunction, leaving mills struggling to stay operational.

“The industry is limping along,” said Tapan Sengupta, Deputy Managing Director of BSRM. “Unless government spending on development projects increases, the sector will not regain its vibrancy.”

Anatomy of a Crisis: How It Unfolded

The decline of Bangladesh’s steel industry mirrors the economic turbulence the nation has faced since 2020.

Global & Domestic Shocks

- Pandemic impact (2020–2021) – Production disruptions and halted projects.

- Russia–Ukraine war (2022–2023) – Scrap prices soared from $400 to $700 per tonne, crippling local manufacturers.

- Currency depreciation – The taka’s weakness inflated import costs.

- Energy inflation – Gas and electricity tariffs rose multiple times, squeezing margins.

- Political transition (2024–2025) – A stalled government and reduced public development spending.

” — a dual-line chart showing steep demand collapse since 2022.")

Banking Breakdown: The Silent Killer

If political instability weakened demand, the banking crisis strangled supply.

Liquidity shortages and international blacklisting of several local banks have made it increasingly difficult to open Letters of Credit (LCs) for raw material imports.

As a result:

-

Scrap and billet imports have slowed,

-

Raw material costs have surged,

-

And mills are running at just 30–40% capacity.

Even though scrap imports rose 10% year-on-year to 4 million tonnes in early 2025 due to lower global prices, the lack of stable financing has offset that advantage.

“We are importing at the same cost as before, but selling at a loss,” said Md. Shahidullah, Managing Director of Metrocem Steel. “If we don’t sell, we default. If we sell, we lose money. The math doesn’t work anymore.”

The Price Collapse

Rebar and MS rod prices in Bangladesh have fallen to their lowest levels in more than three years.

According to BigMint and the Trading Corporation of Bangladesh (TCB):

| City | Rebar Price (Tk/tonne) | Status |

|---|---|---|

| Dhaka | 73,700 | Record low |

| Chattogram | 77,100 | Slightly higher |

| National retail average | 81,000–84,000 | Persistent decline |

While retail buyers welcome the price relief, mills are bleeding cash.

Production costs hover between Tk 88,000–90,000 per tonne, forcing mills to sell below cost by Tk 4,000–8,000 just to maintain cash flow and service bank loans.

“The industry is merely surviving to pay loan instalments,” said Salehin Musfique Sadaf, Director of Strategy at GPH Ispat. “We are operating at a loss, waiting for stability.”

Public Spending Collapse: The Core Problem

The interim government’s policy of reviewing or freezing large-scale projects has led to an unprecedented drop in development spending.

Government data show that in July–August FY2025, only Tk 5,715 crore was spent under the Annual Development Programme (ADP)—a mere 2.36% of the allocation, the lowest execution in 16 years.

That collapse has had a domino effect:

-

Contractors have stalled work,

-

Accounts receivable remain blocked,

-

And mills face a severe cash crunch due to unpaid invoices.

Without strong fiscal revival, experts warn the sector may consolidate into just a handful of dominant players, erasing decades of competition and growth.

Excess Capacity: A Double-Edged Sword

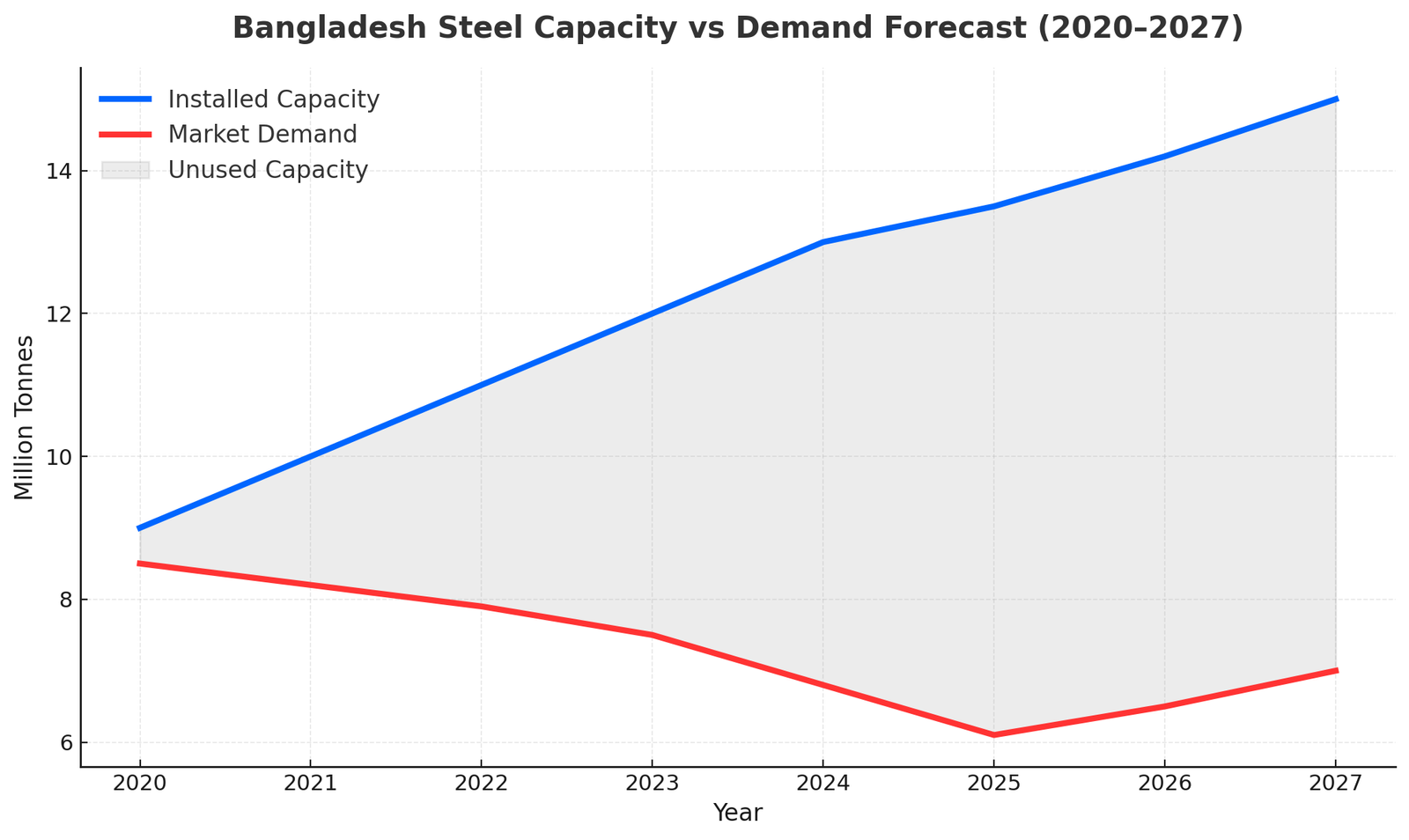

Despite the slump, Bangladesh’s installed capacity continues to grow.

Major producers like Abul Khair Steel (AKS) recently expanded production by 1.6 million tonnes per year, pushing its total capacity to 3 million tonnes annually—making it the largest in the country.

BSRM follows with 2.4 million tonnes, while GPH Ispat, KSRM, and Anwar Steel maintain smaller shares.

| Company | Capacity (Lakh Tonnes) | Market Share |

|---|---|---|

| Abul Khair Steel | 30 | 14% |

| BSRM | 24 | 25% |

| GPH Ispat | 8 | 8% |

| KSRM | 6 | 6% |

Source: BigMint, BSMA, 2025

With industry capacity projected to reach 15 million tonnes by FY2027, insiders warn that investing without demand alignment could destabilize the market further.

“Without aligning supply with demand, further investment is risky,” said Sumon Chowdhury, Chairman of RRM Steel and Secretary of the Bangladesh Steel Manufacturers Association (BSMA).

The Construction & Real Estate Slump

Steel’s health is tied to construction—and both are struggling.

High inflation, rising loan rates, and uncertainty have slowed both public projects and private real estate.

Developers like Concord Group report difficulty securing project finance and declining apartment sales.

Real estate executives warn that smaller firms dependent on bank credit are especially vulnerable.

“When housing slows down, related sectors like steel suffer,” said Anup Kumar Sarker, Senior Executive Director at Concord.

Energy Costs and Tax Burdens

Operational costs have surged due to multiple hikes in gas and electricity prices.

A 5% Advance Income Tax (AIT) on scrap imports further adds pressure, with limited refund options.

Even though raw material costs globally have fallen, the domestic production cost curve keeps rising, making local mills uncompetitive in export markets.

Dependence on Foreign Raw Materials

Bangladesh imports over 80% of its steelmaking inputs—mostly scrap and billets.

China remains the dominant supplier, followed by India, Turkey, and the UAE.

Some mills still prefer European-origin machinery and spare parts, but that dependency increases cost and reduces flexibility.

Ironically, many of those “European brands” have their manufacturing bases in China—a fact often overlooked by risk-averse Bangladeshi buyers.

| Source | Role | Challenge |

|---|---|---|

| China | Main source of scrap, rolls, and spares | Perceived risk of mismatch |

| Europe/USA | OEM-grade machinery | High price, long lead time |

| India | Secondary supplier | Limited quality range |

Signs of Hope: Waiting for FY2027

Despite the gloom, the long-term fundamentals remain strong.

Bangladesh’s per-capita steel consumption is still only 43–45 kg, far below India’s 81 kg or the global average of over 400 kg.

This low baseline suggests enormous potential once economic stability returns.

The World Bank projects GDP growth to rise from 4.8% in FY2025-26 to 6.3% in FY2026-27, with multiple infrastructure projects—bridges, metro extensions, and expressways—ready for relaunch after the February 2026 elections.

“With stability, policy clarity, and an elected government in place, we can expect gradual recovery,” said Sumon Chowdhury of BSMA. “The steel industry has survived crises before—it will rise again.”

The Path Forward: Surviving the Storm, Building the Future

The steel industry of Bangladesh stands today on a fragile bridge—one side weighed down by crisis, the other shimmering faintly with possibility. The road to recovery will not be swift, but it is not beyond reach either.

After years of relentless expansion, mills across the country are now forced to focus on efficiency, cost discipline, and technological modernisation rather than new capacity building. The new watchword is not “growth”—it is “survival through transformation.”

From Expansion to Efficiency

Over the past decade, Bangladesh’s steelmakers raced to expand capacity, hoping to feed an infrastructure-hungry nation.

Now, as demand hovers at barely 60% of total installed capacity (11–13 million tonnes), that strategy has reversed.

Major players—such as BSRM, Abul Khair, GPH, and KSRM—are investing in automation, process optimization, and energy efficiency to cut production costs per tonne.

“We’re not building new plants; we’re strengthening what we already have,” said a senior official at KSRM Group. “The challenge now is to produce smarter, not bigger.”

With most mills operating at 30–40% capacity, survival depends on lowering unit costs while maintaining product quality. Many companies are introducing AI-based process control, waste heat recovery systems, and automated rolling mills to save power and manpower costs.

Waiting for Stability and Stimulus

The entire industry’s mood can be summed up in one phrase: “waiting for stability.”

The interim government, now in power for over 15 months, has virtually halted all new mega projects.

According to the Implementation Monitoring and Evaluation Division (IMED), only 2.39% of the Annual Development Programme (ADP) was implemented in the first two months of FY2025–26—the lowest in 16 years.

Public infrastructure—once the lifeblood of steel demand—is at a standstill.

Private construction and real estate, burdened by high interest rates, uncertain policy, and sluggish consumer confidence, have followed suit.

Yet, hope flickers on the horizon.

The general elections in February 2026 are expected to restore an elected government, paving the way for a revival in ADP spending, foreign-funded infrastructure projects, and private housing investment.

“When political stability returns, construction will normalize—and prices will follow,” said Md Abul Kalam of Bikrampur Auto Re-Rolling Mills.

As one BSMA official put it, “The flame is low, but not extinguished. Steel has always been the skeleton of development—and Bangladesh will need plenty of it again.”

Technology, China, and the Future

China is not just a supplier to Bangladesh’s steel sector — it is the backbone of its industrial ecosystem.

From raw materials to machinery, from capital investment to technology transfer, China’s footprint runs deep across every layer of Bangladesh’s steel value chain.

1. Raw Material Lifeline

Bangladesh’s steelmaking process relies heavily on imported inputs, and China remains the single most critical source.

Chinese suppliers provide a large portion of the scrap, sponge iron, pig iron, ferro alloys, and graphite electrodes that keep local furnaces running.

Without this supply chain, domestic production would grind to a halt.

In 2023 alone, Bangladesh imported over $4.17 billion worth of industrial machinery and metallurgical equipment from China — much of it directly linked to the steel and heavy manufacturing sectors.

Every ton of rebar produced in Chattogram or Narayanganj likely contains components, metals, or parts sourced from Chinese factories.

2. Machinery, Equipment, and Spare Parts

China is also Bangladesh’s largest industrial technology partner, supplying:

-

Rolling mill machinery and automation systems

-

Furnace electrodes and induction components

-

Gear boxes, bearings, and hydraulic spares

-

Cooling systems, valves, and heat-resistant cables

These imports — exceeding $4 billion annually — are not mere trade items but the technological arteries that sustain production.

Even European-origin mills often rely on Chinese spare parts for maintenance and retrofitting because of their availability, affordability, and improved reliability.

3. Strategic Investments and Industrial Zones

Beyond trade, China is now entering Bangladesh’s steel sector as a long-term strategic investor.

A major Chinese consortium has announced plans to invest approximately $2.13 billion to establish a dedicated Iron and Steel Industrial Zone — the first of its kind in Bangladesh — likely to be located near Chattogram or Payra Port.

This zone aims to:

-

Localize scrap processing, billet casting, and rebar rolling

-

Build supporting power and logistics infrastructure

-

Attract downstream industries (such as tools, shipbuilding, and auto parts)

Such a development could fundamentally reshape Bangladesh’s steel supply chain, reducing logistics costs and import dependency while creating thousands of skilled jobs.

4. The Technological Leap

The next phase of the partnership is technological.

Chinese firms are introducing Industry 4.0 innovations — such as AI-based rolling control, automated casting, real-time energy monitoring, and predictive maintenance — to Bangladesh’s mills.

Companies like Bei Sino Forge, Pavone Sistemi (via Chinese engineering partners), and several joint ventures are helping modernize the country’s foundries and melt shops.

This collaboration is shifting the industry’s focus from manual operation to digitally optimized precision manufacturing.

For Bangladesh, the goal is no longer to simply “import from China” — but to learn with China.

5. Long-term Industrial Partnership

Over the last three decades, China and Bangladesh have built an industrial relationship based on trust, affordability, and scale.

This partnership extends far beyond steel — spanning cement, power, fertilizer, shipbuilding, and infrastructure — but steel remains its most critical pillar.

-

75% of new heavy-industrial equipment installed in Bangladesh since 2015 has Chinese origin.

-

Chinese EPC contractors built or upgraded several key facilities, including rolling mills, blast furnaces, and foundries.

-

Technical training programs organized by Chinese metallurgical institutes have begun to produce skilled Bangladeshi technicians.

The result is a form of structured interdependence — Bangladesh depends on China’s industrial base, while China depends on Bangladesh’s growing market for its long-term Belt and Road Initiative (BRI) expansion.

6. Looking Ahead: Beyond Supply to Collaboration

The partnership is gradually evolving from transactional trade to strategic collaboration.

China’s future role in Bangladesh’s steel sector will likely include:

-

Joint R&D centres for metallurgy and material science

-

Green steel projects, using hydrogen-based smelting and solar-integrated power systems

-

Local assembly of Chinese machinery, reducing import costs and delivery times

-

Skill-sharing initiatives, creating a new generation of metallurgical engineers trained under Chinese technology frameworks

This transformation could turn Bangladesh into South Asia’s next steel manufacturing hub, with China as its primary enabler.

7. Summary Table: China’s Role in Bangladesh’s Steel Ecosystem

| Category | Chinese Contribution | Impact |

|---|---|---|

| Raw Materials | Scrap, sponge, pig iron | Keeps local furnaces operational |

| Machinery & Parts | Rolling mills, automation, spares | Drives modernization, reduces downtime |

| Investment | $2.13B planned Iron & Steel Zone | Localized production, job creation |

| Technology Transfer | AI-based systems, predictive maintenance | Enhances productivity, energy efficiency |

| Training & Skills | Metallurgical education & workshops | Builds long-term technical capacity |

8. The Future in One Line

If Bangladesh’s steel furnaces are its heartbeat, then China is the rhythm that keeps it alive.

A Strategic Reorientation

In summary, the path forward for Bangladesh’s steel industry depends on four pillars:

| Priority | Description |

|---|---|

| 1. Stability & Governance | A predictable political climate and consistent project execution. |

| 2. Financial Reforms | Restoring LC credibility and liquidity flow to importers. |

| 3. Cost Optimization | Automation, energy efficiency, and smarter supply chains. |

| 4. Market Confidence | Building investor and consumer trust through transparency and stability. |

Conclusion

The past three years have tested the resilience of Bangladesh’s steelmakers more than any previous crisis. Yet history suggests this sector always finds a way to adapt.

The focus must now shift from expansion to efficiency, from survival to reinvention.

If stability returns—and reform follows—the furnaces of Chattogram and Narayanganj will burn bright again.

Bangladesh’s steel story, though dented, is far from over.

Credit & Source Note

This article synthesizes information from multiple verified and publicly available sources to provide a consolidated overview of the current situation in Bangladesh’s steel industry as of late 2025.

Primary sources include:

- New Age (Bangladesh) – “Steel Industry: Focus on efficiency, cost cutting amid demand slump” by Pimple Barua, published on 24 October 2025.

- The Daily Star (Bangladesh) – “Steel demand weak for three years — BigMint projects a turnaround in FY27”, various interviews with Tapan Sengupta (BSRM), Sumon Chowdhury (BSMA), and Manwar Hossain (Anwar Group), published September 2025.

- The Financial Express (Bangladesh) – “Steelmakers reel from setbacks yet foresee rebound” by Saif Uddin, published 30 September 2025.

- BigMint Bureau (India) – “How is Bangladesh’s steel industry faring a year after the July Revolution?”, published 30 October 2025.

- Trading Corporation of Bangladesh (TCB) – Retail and wholesale price data for MS rods and rebar, Q3–Q4 2025.

- Bangladesh Steel Manufacturers Association (BSMA) – Industry data on capacity, production, and per-capita consumption (2022–2025).

- World Bank and IMF Reports – GDP projections and macroeconomic forecasts for Bangladesh (FY2025–FY2027).

All analytical interpretations, comparative insights, and commentary in this publication are original contributions by Leo Fang and have been written exclusively for Bei Sino Forge Company Blog Series.

0 Comments